November 12, 2018 in Healthcare Analytics

Healthcare technology and analytics: 2018 is a good year overall

SHARE: PRINT ARTICLE: https://doi.org/10.1287/LYTX.2018.06.04

https://doi.org/10.1287/LYTX.2018.06.04

As we are approaching the end of the year I have tried to look back at 2018 in this article. It seemed to me that while the healthcare space is becoming increasingly complex and disruptive, enthusiasm and investments are available in abundance. Is that owing to a roaring economy? Perhaps.

On the policy front, many uncertainties are still plaguing the industry, especially the future of the Affordable Care Act (ACA). Various facets of the law are now being selectively dismantled by the federal government. Will ACA survive the test? The answer is unknown at this time.

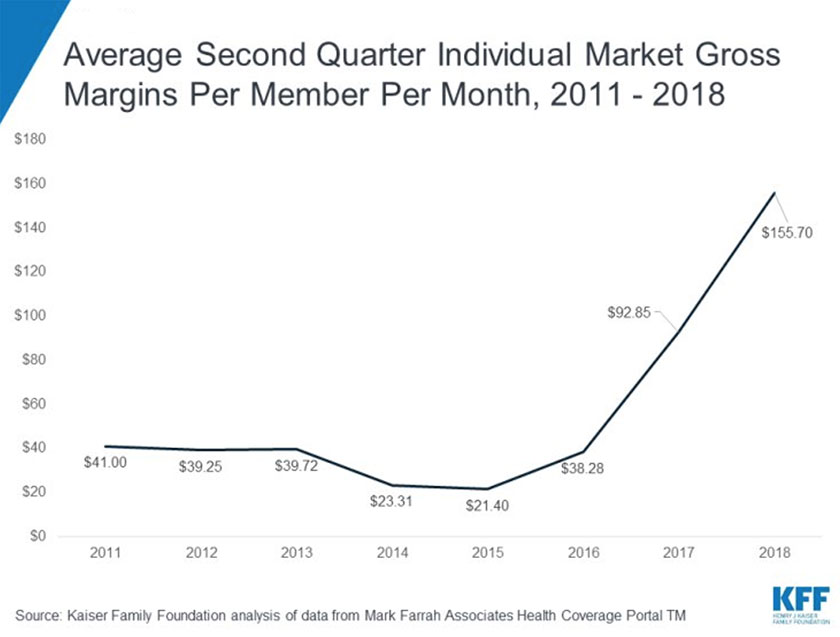

A new report indicates that health insurance companies marketing their plans to the individual marketplace have made significant profits and hence they have lowered the cost of premiums for the next year. Meanwhile, other insurers who left in a hurry during the last couple of years claiming that they were losing money are coming back to the health insurance exchange markets.

So what changed? Insurers increased their prices last year in response to the uncertainty in the marketplace, as well as the news of losing subsidy contribution from the federal government for those who are unable to pay the premiums. They got the subsidy and increased their prices, and therefore ended up with a higher profit margin (see Figure 1).

Figure 1: Insurers in the marketplace enjoyed higher profit margins last year.

Source: Kaiser Family Foundation analysis of data from Mark Farrah Associates Health Coverage Portal™

Coverage for pre-existing conditions, which is the most favored provision of the ACA among consumers, was put on the chopping block in many states. It will be interesting to see how voters in those states respond to the proposal of eliminating mandatory coverage for pre-existing conditions in favor of decreased insurance coverage. Of course, that would help insurers eliminate costly coverages, and for some consumers it might lead to lower premiums. But it would devastate those who go bankrupt due to their uncovered healthcare costs for their pre-existing conditions such as chronic heart disease or cancer.

Congress is also contemplating potential cuts to Medicare and Medicaid coverages after the midterm election in November to balance budget deficits. If that happens it would deliver a severe blow to seniors and the underserved population across the country as many state and county governments depend on federal funding to support those two groups of consumers. It will also be a blow to the healthcare industry overall as Medicaid and Medicare together make up a significant revenue for the healthcare industry.

Disruptions of Business Models: Strange Bedfellows

This year saw some interesting corporate unions in healthcare. Health insurance company Aetna was bought by the retail pharmacy giant CVS. This could be an attempt by CVS to protect them from the growing shadow of Amazon, which has now established themselves in the pharmacy market. In a similar move, health insurance company Cigna acquired retail pharmacy giant Express Scripts.

Amazon can wreak havoc in this space with its super-efficient, technology-enabled operations just like it did in general retail business, forcing former retail giants such as Sears to file for bankruptcy. Amazon also purchased the pharmacy company PillPack this year and hinted at rapidly scaling up that business.

Amazon’s vast data-driven retail enterprise is a huge threat to the pharmacy market. Mergers of health insurance and retail pharmacy companies are geared toward ensuring access to data; CVS can continue to have access to a steady stream of insured patients from Aetna that Amazon might not be able to poach. CVS can also direct those insured patients to its retail clinics.

Will this limit choice for consumers and drive up profit for the combined entity? The American Medical Association believes so. Also, neither Aetna nor CVS is known to be an analytics-driven retailing power like Amazon. It will be interesting to see what transpires in the marketplace and for the consumers at the end.

Emergence of a New Disruptor

Another interesting new entrant in the healthcare space is the joint venture company of Amazon, Berkshire Hathaway and JP Morgan led by Dr. Atul Gawande. The idea is to build a new nonprofit healthcare company that would reduce healthcare cost. So far it is not clear how the cost problem would be addressed, but it is anticipated that data and analytics will play a big role in its operation and price negotiations with Big Pharma. CEOs of three legendary companies will back Dr. Gawande, and each of those organizations is proficient in deep analytics. As healthcare cost reaches 18 percent of the GDP in 2018 and forecasted to reach 20 percent by 2025, all eyes will be on this new company to see what data-driven innovations it would introduce in the marketplace that could eventually help the company achieve its stated goal where many had failed earlier.

Watson’s rude awakening: AI hits the reality speedbump

This year also saw IBM Watson’s image tarnished when news broke about Watson dishing out inaccurate advices to oncologists for cancer treatment, as well as large layoffs that happened within the Watson division this year. In response, IBM tried to defend its position with this blog, where it mentioned that IBM Watson is still used by 230 healthcare organizations worldwide. It is unwise to write them off.

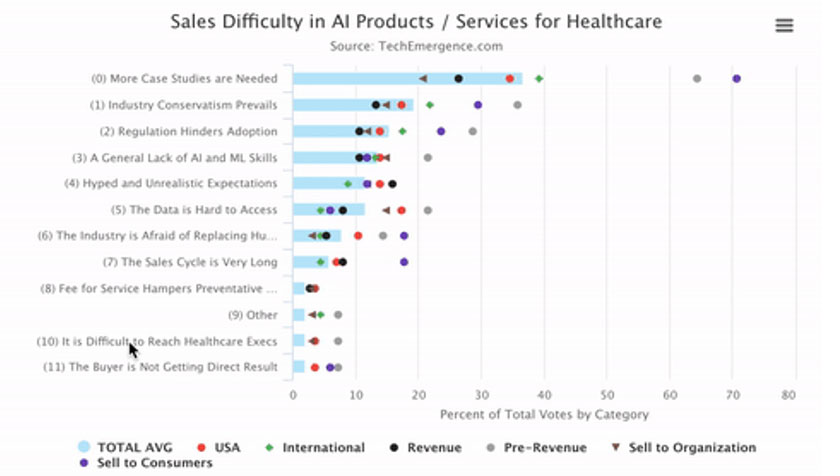

This year also saw Food and Drug Administration (FDA) approve AI-driven diabetic retinopathy detection device - the first of its kind. However, there wasn’t any big movement of AI in healthcare a report based on a survey of healthcare executives. From any given list of 100 AI companies, only 33 percent have the requisite or academic background in science. Of those, only 25 percent are engaged in some meaningful pilots in healthcare. Figure 2 shows the difficulties experienced by AI companies to sell their product or services in healthcare.

Source: TechEmergence.com

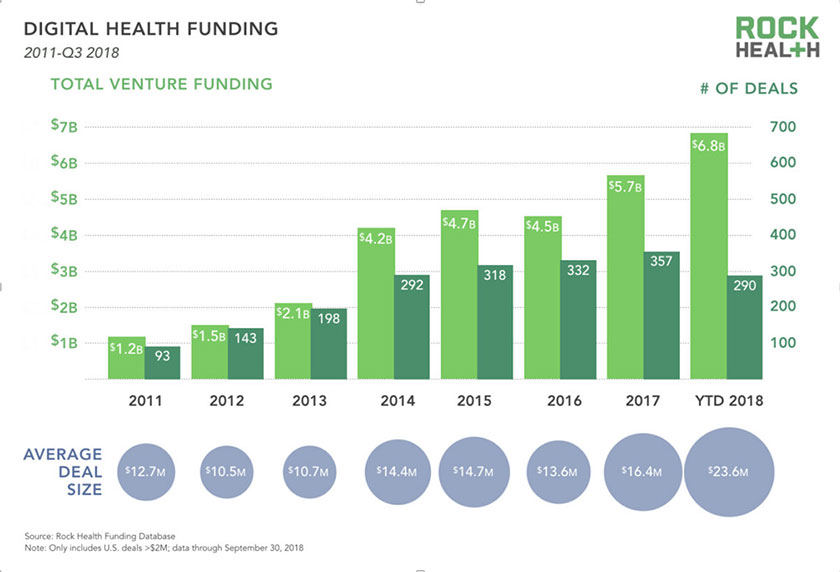

Record Investment in Digital Health

In terms of venture capital investment in digital health technologies and data-driven solutions, 2018 saw about $6.8 billion year-to-date investments through Q3 according to a Rock Health report. That’s a significant jump compared to 2017, which registered $5.7 billion investment the whole year. The money is coming both from traditional venture firms as well as from corporations and healthcare organizations. How many of these startups will survive? Are we seeing enough “needs-driven innovation”? Those

are open questions, but funding is definitely available.

Figure 3: Digital health funding is on the rise.

Source: Rock Health Funding Database

Despite the instability in the policy, world healthcare technology and analytics marketplaces stayed steady overall. The industry is embracing itself for some major disruptions of business models and shifts in 2019 and beyond as previously mentioned. Major changes in the policy world such as cuts to Medicare and Medicaid spending will surely negatively affect the market, along with overall investment. Any recessionary pressure might also put a brake in growth and fund availability. But for now, it seems like 2019 will be a smooth ride. So, let’s raise our glasses; it’s time for a toast.

Rajib Ghosh is the founder and CEO of Health Roads, LLC, a consulting company for enabling digital transformation in healthcare organizations. He has 25 years of technology experience in various industry verticals where he had management roles in software engineering, data analytics, program management, product management, business operations and strategy development. Ghosh spent a decade and half in the U.S. healthcare industry as part of a global ecosystem of medical device manufacturers, medical software vendors, telemedicine and telehealth solution providers. He’s held senior positions at Hill-Rom, Solta Medical and Bosch Healthcare. His recent work includes leading data-driven digital transformation in the public health space, including county-level healthcare agencies and organizations focused on underserved populations.

([email protected])